RISK MANAGEMENT

Risks: Assessment and Alleviation

We work with the understanding that markets are inherently risky. We see possibility of permanent capital erosion or of poor returns in the long run as the central risk factor and strive to minimize this risk - as our first goal. Magadh Capital does not see stock price dip due to short term volatility as a measure or indicator of risk.

Our investment philosophy and style have been shaped by our focus on alleviation of risks in our pursuit for wealth creation for our investors. Accordingly, our first principle is “Do not lose money”. Our investment process by its nature is designed to assist us in identifying key risk factors, in trying to estimate the range of probabilities for various risk factors, and in thinking of impact of those risk factors. At the same time, while we score well on the scale of risk aversion, we are not loss averse over near term especially if we are convinced regarding long term opportunities.

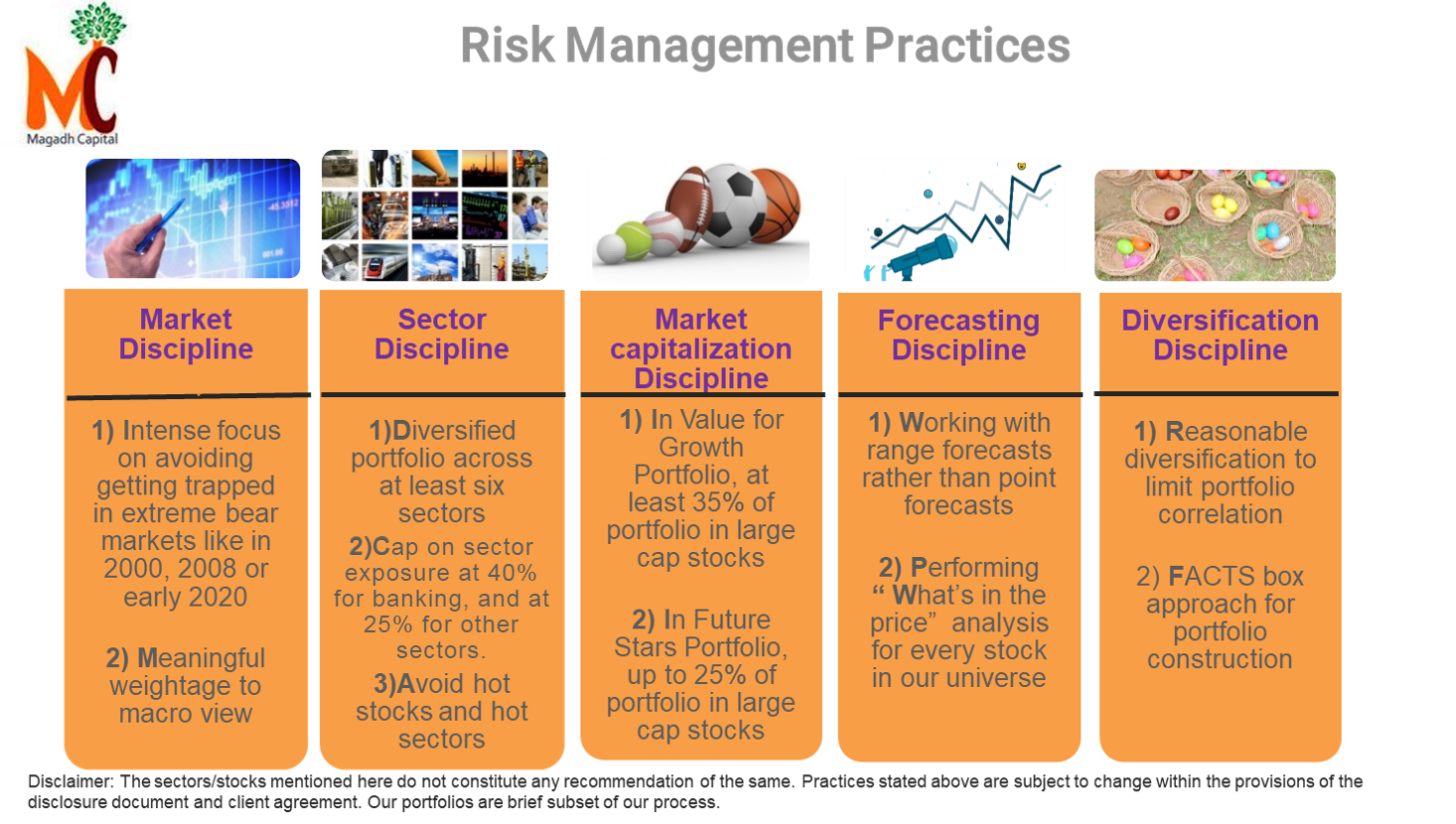

At the top-down level, we are extremely wary of getting caught in deep and

prolonged bear markets like in 2000, 2008, or in early 2020. If we sense that a

vicious bear market is likely ahead, we aggressively shift to cash. However, we

never try to time the market. We believe markets can decline (or rise) by 10-15%

at any point in time without any genuine reason – and that they are inefficient

especially in short term. Hence, we do not try to outguess such fluctuations.

Similarly, we do not sell a stock with the hope to buy it later at 10-15% lower

levels. On the other hand, if, say, we expect, with a 70-75% probability, the

market to decline by 20-25% then we sell out of our holdings aggressively.

Hence, apart from our core focus on bottom-up analysis we spend quite some

time on subjects like macroeconomics, geo-politics, trade pattern, infrastructure

development, income growth etc.

The most reliable way to risk alleviation, in Magadh Capital’s view, is to a) select

stocks with low probability of capital erosion or of poor returns in the long run –

here we think a lot of about margin of safety, and b) create a properly

diversified- across sectors, business models, themes, business cycles, cash flow

growth etc- portfolio with low correlation.

Fundamental research is our most potent tool to identify and assess risks

associated with a stock and a sector. The kind of stocks – those with robust

corporate governance, good management, strong competitive positioning, and in

many cases strong balance sheet – that we own in our portfolio curbs risks to

our portfolio.

We ensure sizeable margin of safety at the time of our stock purchasing

decisions which provides another source to mitigate risks to our portfolio.

In addition, a longer-term horizon – that we work with - disincentivizes sudden

rush of adrenaline that often increases the probability of a risk factor playing

out.

Potent diversification is another important tool that we use for risk mitigation.

Our portfolios are diversified on the lines of sectoral drivers, business traits and

market capitalization. Our FACTS box approach of portfolio construction helps us

perform optimal level of diversification.

For risk assessment we routinely monitor measures like standard deviation and beta. However, we do appreciate the limitations of these techniques. First, these are historical measures and may or may not be good indicators of risks in future. Further, risk assessment exercise based on these measures makes some assumptions (some key ones being that bell normal curve properly represents stock price movement, and that stock prices are deterministic in nature) that may not be perfect.

Accordingly, we rely more on qualitative analysis for future risk estimation in the

backdrop of Magadh Capital’s investment horizon and risk definition, and on

steps like

• having not less than 10 stocks in the portfolio,

• active monitoring of drawdown levels to look for mistakes or meaningful change in investment environment for some stock